You deserve the best price + best advice + best mortgage experience.

Welcome to the Excellent Loan Process!

A rate is great, but you deserve more than just a rate and monthly payment. You also deserve expert mortgage advice and a great experience. Purchasing a home is often the largest investment of your life, and with the Excellent Loan Process (ELP), you get guidance and support before, during, and long after you close.

Leo Anzoleaga is the Senior Vice President of Residential Lending at Luminate Bank and a Certified Mortgage Planning Specialist (CMPS), a title that only 7% of mortgage professionals have. He understands that your mortgage is one piece of your financial situation, and his team provides guidance on how it fits into your short- and long-term financial plan.

Do your due diligence and ask every lender you interview for their written process so you can fully understand how they will support and guide you through your mortgage experience. Here's ours.

The Leo Anzoleaga Team worked with the world-renowned Ritz-Carlton Leadership Center to bring you the best-in-class customer experience.

How does the Excellent Loan Process (ELP) work?

As you interview different lending partners, I encourage you to ask these four questions to determine which team is the best fit for you. The Leo Anzoleaga Group shows you what to expect before, during, and after your Excellent Loan Process (ELP) below!

Have you already decided to work with our team? Let us know and we'll schedule your initial consultation!

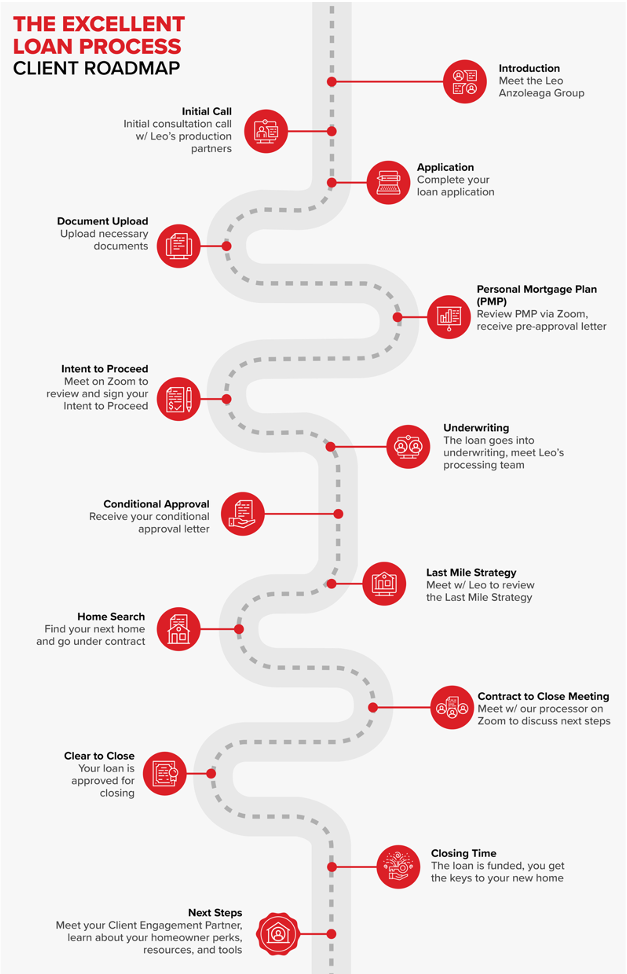

Before the Loan

Step 1

Introduction to the Leo Anzoleaga Group.

My team and I here are honored to meet you. After you are introduced to us, we send you a quick email that tells you more about what you can expect on the mortgage side before, during, and after your homebuying process.

About the Leo Anzoleaga Group: Leo Anzoleaga is a Certified Mortgage Planning Specialist with more than 20 years of experience in the mortgage industry. He has built his successful mortgage business through relationships, strategy, and execution specializing in helping homebuyers and their agents stay competitive in the real estate market.

Step 2

Initial consultation call with Leo's production partners.

You will schedule a free 15-minute call with one of my production partners. They will gather details about your real estate needs, goals, and purchase timing. This step is critical for building a personalized mortgage plan and finding the best financing option for you.

Haven’t scheduled your free consultation yet? No problem. You can easily schedule a time that is convenient for you.

Step 3

Fill out the loan application online.

When you fill out your loan application online through our secure portal, you will submit your financial details and we’ll start the pre-approval process. There's no commitment in applying; it's just the most efficient way for us to give you accurate information in your personalized mortgage plan.

Employment

Income

Assets

Debts

Property Information

Credit History

As you may know, we do pull your credit after you apply online. But what you may not know is how we calculate your credit score (which may be different from other types of lenders). Learn more in the video below.

We're always a phone call away if you need help or have questions or concerns along the way.

Step 4

Upload necessary documents.

Our lending portal is easy to use. In order to give you the best price and advice, we need all necessary documents uploaded to help paint a complete picture. We are looking for documentation to help us understand your:

Employment

Income

Assets

Debts

Property Information

Credit History

Step 5

Present Personalized Mortgage Plan via Zoom and receive pre-approval letter.

Leo walks you through your Personalized Mortgage Plan (PMP) during a Zoom meeting or private video. Your PMP shows you the numbers, gives you more details about your approved loan amount, estimates for monthly payments and fees, and shares insights into how we proactively prepare for your offers and negotiations. Afterward, you will receive an email with your pre-approval letter.

Step 6

Intent to Proceed conversation via Zoom then sign your Intent to Proceed.

One of your best competitive advantages when working with the Leo Anzoleaga Group is having a conditionally approved loan before you make an offer on a home. But before we submit your loan into underwriting, we will ask you to review and sign your Intent to Proceed to let us know that you want to move forward with our team. Don't worry — we will discuss this beforehand and then walk through it again during this Zoom meeting.

Curious about the history of underwriting? We got you.

Step 7

Meet Leo's processing team and the loan goes into underwriting.

When you sign your Intent to Proceed, you will also meet our dedicated processor, who submits your loan application into underwriting and helps manage that process. They may reach out to you to ask for clarification or additional documentation, so it is helpful to put a face to a name (and email).

Step 8

Receive your conditional approval letter.

We send your conditional approval letter via email! Keep in mind that all approvals are subject to satisfactory appraisal and title, and there should be no material changes to your financial status.

Once the Leo Anzoleaga Group issues the loan commitment, we will update the letter every 90 days as needed until you are under contract because our ultimate goal is to only have the title, appraisal, insurance, and condo documents (if applicable) pending at any given moment. This planning and preparation allows us to execute your loan when the opportunity to go under contract arises.

During the Loan

Step 9

Last Mile Strategy meeting with Leo via Zoom.

By now you have been looking at homes with your agent, eliminating properties using the Rule of 85. At this time, you meet with Leo to walk through various proactive strategies his team is preparing behind the scenes to solve the "Last Mile Problem." Questions he helps you answer during this meeting may include:

How long to breakeven if you have to bid over the asking price?

What do you do if the appraisal comes in lower than the loan amount?

What contingencies and closing credits could we negotiate with the seller?

How does this neighborhood impact this property's value over time?

How do different down payments amounts affect the numbers?

Send Leo the address of properties that fit your criteria, and he will update the numbers for you and your real estate agent.

Step 10

Find your next home and go under contract.

It's time to make an offer on a property! Now what?

You and your agent consult with my team as you draft your offer to the seller. This is when we use our network to communicate with the seller's agent and deploy the Last Mile Strategy to craft a competitive contract and negotiate if the seller counters.

Once under contract, we work on locking in interest rates and moving your file back to underwriting to get the loan disclosed, signed, and approved. We will send you information and examples of the documents you should review so we can move quickly in the next few steps.

Step 11

Contract-to-Close meeting with our processor via Zoom to discuss next steps.

At this meeting, the loan is disclosed, signed, and approved. The Loan Processor will send you the Initial Loan Disclosure, which includes the loan terms, your projected monthly payments, and how much you will pay in fees and other costs to get your mortgage (closing costs).

After reviewing your Initial Disclosure, you can look forward to a final walkthrough of the home, instructions on wiring your closing money to the title company, and closing day itself.

After the Loan

Step 12

Clear to close.

We have reached a huge milestone: you are clear to close! At this point, you have met all of the requirements and conditions to close on your mortgage. You will receive your Final Closing Disclosure via email.

Step 13

Closing time! The loan is funded and you get the keys.

Celebration time! You meet, in person or remotely, with your settlement agent to close on the home. At this point, you review and complete all of your closing documents. After you and the seller close, you can expect to get the keys to your new home.

Step 14

Meet Leo's client success team to learn about your free homeowner perks, resources, and tools.

You will also be enrolled in our complimentary Mortgage Under Management program, which allows you to take advantage of savings over the lifetime of your mortgage and meet with our experts for annual reviews of your investment. Your transaction came to a close, but your homeowner perks have just begun! At this point, you will be introduced to your personal client success manager and your free homeowner financial tools and resources.

The best price, advice, and mortgage experience for life.

Ready to work with the

Leo Anzoleaga Team?

Email us to get started.

FHA Closing Disclosure

A closing disclosure for an FHA loan is the final document provided at least three business days before closing that details the actual loan terms, monthly payments, closing costs, and FHA-specific items like mortgage insurance premiums, confirming the final numbers you'll pay to complete your home purchase.

Sample Closing Disclosure

FAQs

What is an FHA initial loan disclosure and when do I receive it?

The FHA initial loan disclosure is a document that outlines the key terms and costs of your FHA loan. Lenders are required to provide this within three business days of receiving your complete loan application, giving you early transparency about loan terms before you're committed to the loan.

What information is included in the FHA initial loan disclosure?

The disclosure typically includes your loan amount, interest rate, monthly payment estimates, closing costs, annual percentage rate (APR), loan terms, and any FHA-specific requirements like mortgage insurance premiums. It also details prepayment penalties if applicable and other fees associated with the loan.

How does this differ from the Loan Estimate I receive?

The FHA initial loan disclosure often refers to the standardized Loan Estimate form required by federal law. For FHA loans, this document includes FHA-specific information like upfront mortgage insurance premiums and annual mortgage insurance costs that may not be as prominent in conventional loan estimates.

Can the terms in the initial disclosure change before closing?

Yes, some terms can change, but there are limits. Under federal regulations, certain fees cannot increase at all, others can increase by up to 10%, and some can change without restriction. If significant changes occur, you may receive a revised disclosure and potentially have additional time to review the changes.

What should I do after receiving the FHA initial loan disclosure?

Review all terms carefully, compare them with other loan offers if you're shopping around, ask your lender questions about anything unclear, and ensure you understand the total cost of the loan including FHA mortgage insurance. You're not obligated to proceed with the loan just because you received the disclosure.

Conventional Closing Disclosure

A closing disclosure for a conventional loan is the final document provided at least three business days before closing that details the actual loan terms, monthly payments, closing costs, and any private mortgage insurance (if applicable), confirming the final numbers you'll pay to complete your home purchase.

Sample Closing Disclosure

FAQs

What is private mortgage insurance (PMI) and why does it appear on my conventional loan disclosure?

PMI is insurance that protects the lender if you default on your loan, and it's required on conventional loans when you put down less than 20%. Your disclosure will show both the upfront PMI cost (if applicable) and the monthly PMI payment, which can add $100-300+ to your monthly payment depending on your loan amount and down payment. Unlike FHA loans where mortgage insurance is permanent in many cases, conventional PMI can be removed once you reach 20% equity in your home.

Why might my interest rate be higher than advertised rates I've seen?

The interest rate on your disclosure reflects your specific financial profile, including credit score, debt-to-income ratio, loan amount, and down payment. Conventional loans have risk-based pricing, meaning borrowers with lower credit scores or higher risk factors pay higher rates. The advertised rates you see are typically for borrowers with excellent credit (740+ scores) and substantial down payments.

Can I remove PMI from my conventional loan and when?

Yes, unlike FHA loans, conventional loan PMI can be removed. Your disclosure should reference this benefit. You can request PMI removal once you reach 20% equity through payments or home value appreciation, and it automatically terminates at 22% equity. Some borrowers choose to refinance or make extra principal payments to reach the 20% threshold faster and eliminate the monthly PMI cost shown in their disclosure.

How is FHA and Conventional loan disclosures differ?

There are a few key differences between these loans and their disclosures.

FHA disclosures show both an upfront mortgage insurance premium (UFMIP) of 1.75% of the loan amount and an annual mortgage insurance premium (MIP) that's divided into monthly payments. The annual MIP typically ranges from 0.45% to 1.05% of the loan amount depending on the loan-to-value ratio and loan term. Conventional loan disclosures show private mortgage insurance (PMI) only if you put down less than 20%, and the cost structure is different - sometimes upfront, sometimes monthly, or a combination.

FHA disclosures reflect that mortgage insurance is typically permanent for the life of loans with less than 10% down payment, or lasts 11 years for loans with 10% or more down. Conventional loan disclosures show that PMI can be removed once you reach 20% equity and automatically terminates at 22% equity, giving borrowers a clear path to eliminate this cost.

FHA loan disclosures show a minimum down payment requirement of just 3.5%, making homeownership more accessible to borrowers with limited savings. Conventional loan disclosures typically show higher down payment requirements - usually 3-5% for first-time buyers and 5-20% for others, with many programs requiring more substantial down payments to get the best rates.

FHA disclosures reference FHA loan limits that vary by county and are generally lower than conventional loan limits. They also indicate the loan is government-insured through HUD. Conventional loan disclosures show conforming loan limits (currently $766,550 in most areas for 2024) and indicate the loan may be sold to government-sponsored enterprises like Fannie Mae or Freddie Mac, but isn't government-insured.

FHA loan disclosures often show more favorable terms for borrowers with lower credit scores, as FHA loans are designed to be accessible with scores as low as 580 (or 500 with 10% down). Conventional loan disclosures typically reflect more significant risk-based pricing adjustments, meaning borrowers with lower credit scores see notably higher interest rates and fees. FHA rates are generally more consistent across different credit profiles, while conventional rates can vary dramatically based on creditworthiness.

VA Closing Disclosure

A closing disclosure for a VA loan is the final document provided at least three business days before closing that details the actual loan terms, monthly payments, closing costs, and VA-specific items like the funding fee, confirming the final numbers you'll pay to complete your home purchase with no down payment or mortgage insurance required.

Sample Closing Disclosure

FAQs

How is a VA loan disclosure similar to loan disclosures for FHA and Conventional loans?

All three loan types use the same standardized Loan Estimate form mandated by the Consumer Financial Protection Bureau (CFPB). Lenders must provide this disclosure within three business days of receiving a complete loan application, regardless of loan type. The basic format, layout, and timing requirements are identical across VA, FHA, and conventional loans.

The fundamental loan details are presented the same way in all disclosures: loan amount, interest rate, monthly principal and interest payment, loan term, and annual percentage rate (APR). The method of calculating and displaying these core elements follows the same federal standards regardless of whether it's a VA, FHA, or conventional loan.

All loan disclosures break down closing costs into the same standardized categories: origination charges, services the borrower cannot shop for, services the borrower can shop for, taxes and government fees, and other costs. The three-day review period and rules about when lenders must provide revised disclosures due to changed circumstances apply equally to all loan types.

All three loan types must comply with the same federal Truth in Lending Act requirements, meaning they display the same required disclosures about finance charges, payment schedules, and the right to cancel. The APR calculation methodology and disclosure requirements are standardized across all loan types.

Borrowers receive the same federal protections regardless of loan type, including the right to shop for certain services, protection against excessive fee increases between initial disclosure and closing, and the same appeal processes for disputes. The three-business-day waiting period before closing and the borrower's right to receive final closing documents in advance apply universally to VA, FHA, and conventional loans.

What makes a VA loan disclosure different from FHA and conventional loan disclosures

VA loan disclosures include VA-specific benefits and requirements that don't appear in other loan types. Most notably, VA loans don't require mortgage insurance, so you won't see PMI or MIP costs that appear in conventional and FHA disclosures. Instead, you'll see the VA funding fee, which is a one-time upfront cost that can be financed into the loan. The disclosure also highlights VA-specific benefits like no down payment requirement and no prepayment penalties.

What is the VA funding fee shown in my disclosure and how does it compare to other loan insurance costs?

The VA funding fee is a one-time charge that ranges from 1.25% to 3.3% of the loan amount, depending on factors like military service type, down payment, and whether it's your first VA loan use. Unlike FHA's ongoing mortgage insurance premium or conventional PMI that you pay monthly, the VA funding fee is typically rolled into your loan amount as a lump sum. Veterans with service-connected disabilities are exempt from this fee entirely.

How do VA loan closing costs differ in the disclosure compared to FHA and conventional loans?

VA loan disclosures will show restrictions on closing costs that don't exist with other loan types. The VA limits what closing costs veterans can pay, prohibiting charges for things like loan processing fees, underwriting fees, and document preparation fees that commonly appear in FHA and conventional loan disclosures. This often results in lower total closing costs for VA borrowers, though some costs may be shifted to the seller or lender.

Why don't I see mortgage insurance listed like I would on FHA or conventional loan disclosures?

VA loans are guaranteed by the Department of Veterans Affairs, eliminating the need for private mortgage insurance (PMI) found in conventional loans or mortgage insurance premiums (MIP) required for FHA loans. This means your monthly payment disclosure will be lower than comparable FHA or conventional loans since you won't have ongoing insurance costs, though you may have the one-time VA funding fee instead.

What VA-specific requirements or benefits should I look for in my loan disclosure?

Your VA loan disclosure should clearly show that no down payment is required (unlike most conventional loans), confirm there are no prepayment penalties, and may reference VA appraisal requirements that are more stringent than conventional loans. The disclosure should also indicate your VA loan entitlement usage and remaining benefit, information that's unique to VA loans and doesn't appear in FHA or conventional loan documents. Additionally, look for the Certificate of Reasonable Value (CRV) requirements that are specific to VA financing.

Why don't I see a down payment requirement on my VA loan disclosure?

VA loans offer 100% financing, meaning qualified veterans can purchase a home with no down payment. This is one of the key benefits of VA loans and why you won't see a down payment line item that appears on most other loan disclosures. However, you can still choose to make a down payment to reduce your loan amount and potentially lower your VA funding fee.

What is the VA funding fee shown on my disclosure and can it be waived?

The VA funding fee is a one-time cost that helps sustain the VA loan program for future veterans. It typically ranges from 1.25% to 3.3% of your loan amount and can usually be rolled into your mortgage. The fee is completely waived if you have a service-connected disability rating, are receiving VA disability compensation, or are the surviving spouse of a veteran who died from a service-connected disability.

Why are my closing costs lower than expected compared to other loan types?

VA regulations prohibit veterans from paying certain closing costs that are common with other loans, such as loan processing fees, underwriting fees, and document preparation charges. Your disclosure will only show VA-allowable closing costs, which helps keep your out-of-pocket expenses lower. The seller or lender typically absorbs the prohibited costs.

Do I need to budget for mortgage insurance like other borrowers?

No, VA loans don't require private mortgage insurance (PMI) or mortgage insurance premiums (MIP) that you see with conventional and FHA loans. The VA guarantee eliminates this need, so your monthly payment disclosure won't include ongoing insurance costs. This can save you hundreds of dollars per month compared to other loan types.

What does "VA entitlement" mean on my disclosure and how does it affect my loan?

VA entitlement is your available loan guarantee benefit, which determines how much you can borrow without a down payment. Your disclosure may reference your entitlement usage - most veterans have $36,000 in basic entitlement plus additional entitlement based on local loan limits. If you've used VA benefits before, your remaining entitlement will determine whether you need a down payment for your current purchase.

Can I pay off my VA loan early without penalties?

Yes, VA loans cannot have prepayment penalties, and this consumer protection should be clearly stated in your disclosure. You can make extra payments or pay off your entire loan early without any fees, unlike some other loan types that may include prepayment penalty clauses.

What is a Certificate of Reasonable Value (CRV) and why is it mentioned in my disclosure?

The CRV is the VA's appraisal of the property's value, and it sets the maximum loan amount the VA will guarantee. Your disclosure may reference this requirement because VA loans cannot exceed the CRV amount, and the property must meet VA's minimum property requirements for health and safety.